Alfalfa and grass hays produced in the US ending up feeding dairy cows in Riyadh or Bengbu? Who would have thought?

What was once a minor curiosity has fully emerged as a major market for western US hay producers.

Hay has been traditionally been fed to animals very close to home and it still is in most of the United States (Figure 1). However, US and world trade in hay products (primarily alfalfa and grass hay and cubes) has increased dramatically over the past decades due to advanced methods of mechanical handling and inexpensive international freight rates. The high quality of western-grown alfalfa and grass hay has been especially demanded by foreign buyers.

Figure 1. Historically, technology has limited the transport of hay products (left, circa 1890), while modern methods have improved the ability to ship bulky hay products long distances (right 700 kg. hay bales in Arizona awaiting export to the Middle East).

But hay export is not without controversy. Technical issues, and problems associated with the 2018 Trade Disruption with China has affected the international hay trade in recent years.

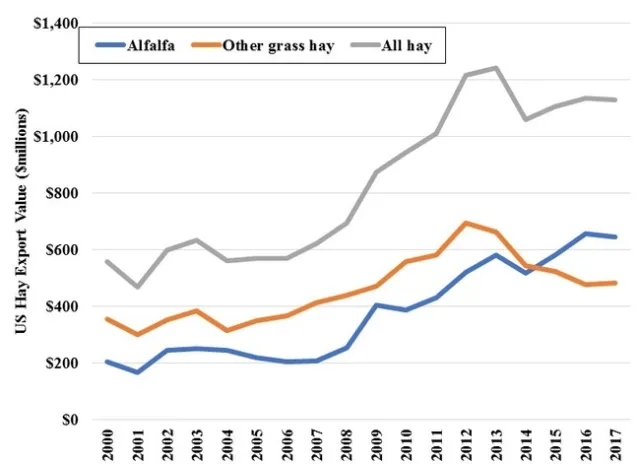

Figure 2. Inflation Adjusted Value of Annual US Hay Exports, 2000-2017 (Base Year = 2010)

TRENDS IN THE HAY TRADE

Alfalfa Exports have Tripled. Over the course of the last two decades, the value of US alfalfa hay exports from the US has tripled, increasing from around $200 million to over 600 million. All hay (alfalfa and grasses have approximately doubled, increasing to $1.2 billion (Figure 2).

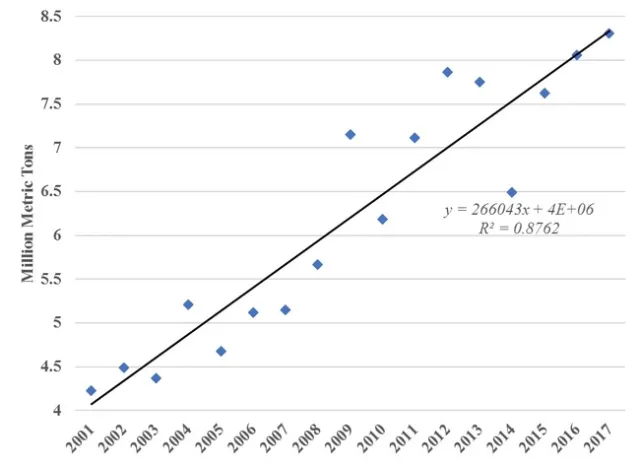

On the world stage, the sum of world hay trade quantities has approximately doubled over the past 16 years, increasing at the average rate of about 266,000 MT/year each year (Figure 3), with strong increases in exports into Asia and the Middle East.

Figure 3. Global Trade in Alfalfa & Grass Hays, 2001-2017 (source: ITC Trade Map).

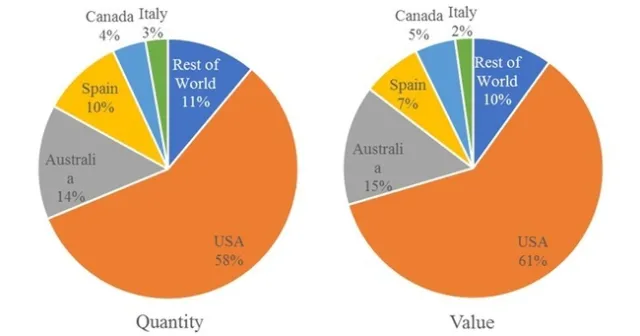

US Leads. The United States is the leading hay export country, followed by Australia, Spain, Canada and Italy (Figure 4). While some forage is exported from other countries (e.g. Argentina, Sudan, Morocco, France, Germany, Mongolia, Romania), these make up less than 11% of the world trade, according to the International Trade Center.

Figure 4. Global Exports of Alfalfa and Grass Hays by Country Share of Quantity and Value, 2017. Source:ITC Trade Map.

What is Exported? While alfalfa dominates hay markets in many countries, high quality grass hays (timothy, sudangrass, bermudagrass, oat hay, kleingrass) make up a substantial portion of exported hay, nearly 50% from the US. Australia's exports are nearly all ‘oaten' grass hay.

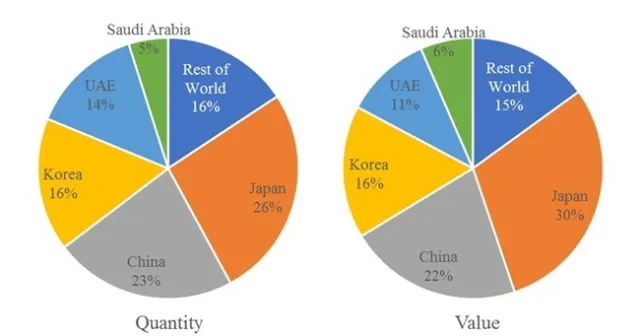

Figure 5. Global Imports of Alfalfa and Grass Hays by Country Share of Quantity and Value, 2017. Source: ITC Trade Map.

Where is the Demand? The major demand for imported forage crops is in Asia, led by Japan, China and Korea (Figure 5), followed by Middle Eastern countries of Saudi Arabia and the UAE. These countries have expanded or improved their dairy and beef production and often do not have adequate space or water resources for high quality pasture, silage, or hay production.

Figure 6. Changes in international markets for US-grown alfalfa hay, 2007-2017.

Shifting Markets. An important development in the past decade has been the emergence of China and Middle Eastern markets. These rose from negligible amounts in 2007 to millions of MT per year in 2017 for alfalfa (Figure 6). This increase was driven primarily by rapid expansion of modern dairy farms in China and Korea, and limitations of water resources in Saudi Arabia and the UAE. Water limitations and distance to markets are also major limitations in China. In 2007, about 85 percent of US exports went to Japan and Korea. Over the past decade, China has become the largest importer of US alfalfa, receiving over 40 percent of total US alfalfa exports. Shipments to Japan and Korea have grown as well, but Korea has been surpassed by Saudi Arabia and the UAE (Figure 6). The Middle East is second to Asia as the most important market for exported US alfalfa. Although experts disagree about the extent of the potential increase in Saudi demand, amounts may eventually reach over 1-3 million MT.

Domestic Acreage has Fallen. Despite this export growth, alfalfa production in the US has fallen over the same period, nationwide and in those areas dominating the export market. The seven western states of Arizona, California, Idaho, Nevada, Oregon, Utah, and Washington are the primary sources of alfalfa for export. These states produced close to 22.5 million MT in 2002, a peak year, but in 2017 produced only 18.2 million MT, a decline of nearly 20%. This was due primarily to a steady decrease in California, while production in the other western states has been relatively steady. Competition from other crops and water resource limitations have been key factors in this decline in western states.

Impacts on Domestic US Markets. Exports as a percentage of production has increased, but is still minor compared with many agricultural products. While the percentage of the national US crop exported remains below 6% for alfalfa and below 3% for grass hays, the equivalent percentage of production exported from the 7 western states exceeded 17% for alfalfa and 41% for grass in 2017. In specific regions of production, exports dominate the hay market, particularly in the Columbia basin region of Washington State and the Imperial Valley in California. This rapid rise in export demand has been welcomed by cash hay growers, but regarded as a negative by domestic dairy and other livestock hay buyers, who have had to compete for forage supplies with foreign buyers.

CHALLENGES

Recent US/China Trade Turmoil. The trade disruption that has developed between the US and China in the summer of 2018 has had an impact on the hay trade. China had become the number one destination for US alfalfa over the course of the last ten years, growing from only 3,000 metric tons of imports in 2007 to over 1.2 million in 2017 (Figure 6). In response to US trade actions, China has recently implemented retaliatory tariffs and other less formal measures on US agricultural products, including an increase the alfalfa hay tariff by 25 percentage points, resulting in a 32 percent import tax. Evidence shows that hay exports to China are down substantially in late 2018 and early 2019,and is probable that this tariff increase (and other informal discouragements to import from the United States) could be sufficient to block most imports of US alfalfa. In that case, the impact of these tariffs on the alfalfa market are likely to be substantial. However, this effect could be mitigated if other markets for US forage are identified or the tariffs do not completely block US forage from entering China. If current negotiations underway between the United States and China are fruitful, U.S. exports could bounce back quickly. Nonetheless Chinese buyers may keep their trade options open and diversify their supply portfolio given the uncertainty of US and China policy.

Sensitivity to Genetically Engineered Traits. Two GE traits are now commercialized in alfalfa grown the United States: Roundup Ready (glyphosate tolerance) and HarvXtra (a reduced lignin trait). At this writing, neither trait is permitted for production in or import into China. In other countries, the traits may be permitted in some countries and not in others. Some GE alfalfa has been exported to Japan and other countries. However, growers for export to China must grow a conventional alfalfa variety that is free of the trait, even in a very small amount. Export companies in the US routinely test export hay for Low Level Presence (LLP) of the Roundup Ready trait and will reject hay with even a small amount (e.g. 0.1%) of LLP. This may change in the future if China approves these traits. Other countries either allow a trait to be imported (as with Japan), require a statement of ‘non-GMO” or do not routinely test. Some importing companies reject GE hay due to sensitivity of their customers who do not want GE traits (even if they are permitted by import regulations).

Controversies: The Water Link. Water resource availability in many parts of the world plays a key part in the demand, as well as the supply, for international trade in forage crops. UAE and Saudi Arabia, both water-poor countries, have made domestic policy decisions which aim to stop the utilization of groundwater for forages. Saudi Arabia has made a decision to stop almost all production of hay domestically by 2018-19. Saudi hay production had reached about 4 million MT. UAE had made the same decision 6 years earlier. Saudi Arabia imported 685,000 MT in 2016 and over a million MT in 2017 (up from zero 5 years ago).

The demand for hay imports into China is similarly driven by lack of land and water resources for domestic production, as well as distance of hay areas from the dairies and unfavorable weather for hay making. The vast majority of the exported hay from the United States is from irrigated regions which are ideal for making quality hay because of dry summers. However, California and other parts of the West also face substantial limitations and competition for water resources. This is also true in Australia, Spain, Italy, and North Africa. The export of hay has become political to some activists and campaigners as complaints about ‘trade in virtual water' are raised (see blog: Is Shipping Water to China in Hay Immoral?. https://ucanr.edu/blogs/blogcore/postdetail.cfm?postnum=8825

Regardless of the politics, it is clear that sustainability of water use must be a key component of forage production wherever grown or consumed.

SUMMARY

The international trade in forages (primarily alfalfa and grass hay) has risen from a minor to a major component of hay markets in western US States. The large production areas such as western US, western Canada, Australia, Spain, and Italy have increasingly exported to Asian and Middle Eastern markets, predominantly China, Japan, Saudi Arabia, and the UAE. US is the lead exporter, and exports are now greater than the equivalent of 17% of the alfalfa and 41% of the grass hays produced in the 7 western US states. Export markets demand high quality forages, whether alfalfa or grass hay types, which favor exporting production regions with good weather and technology for hay making. Improvements in hay packaging, inexpensive ocean transport systems, resource limitations, and imbalance of world trade have been major components driving this trend.